On August 3, 2017, the Financial Accounting Standards Board (FASB) issued an exposure draft of a proposed new Accounting Standards Update (ASU) titled Clarifying the Scope and the Accounting Guidance for Contributions Received and Contributions Made. The FASB is accepting comments on the exposure draft through November 1, 2017.

The FASB has identified that many entities have had difficulty in characterizing grants and similar contracts with resource providers as either exchange transactions or contributions and in distinguishing between conditional and unconditional contributions. Therefore, the proposed ASU is designed to clarify and improve the accounting guidance for contributions received and contributions made.

The amendments in the proposed ASU would assist entities to:

- Evaluate whether transactions should be accounted for as contributions (nonreciprocal transactions) or as exchange (reciprocal) transactions; and

- Distinguish between conditional and unconditional contributions.

Distinguishing between contributions and exchange transactions determines which guidance is applied. For contributions, an entity should follow the guidance in Subtopic 958-605 of the Accounting Standards Codification (ASC), whereas for exchange transactions, an entity should follow other guidance, such as the new revenue recognition guidance that will be effective in the next couple of years.

Once a transaction is deemed to be a contribution, entities have noted that it can be difficult in practice to distinguish between conditional and unconditional contributions, particularly when an entity receives assets accompanied by certain stipulations but with no specified return policy for when the stipulations are not met.

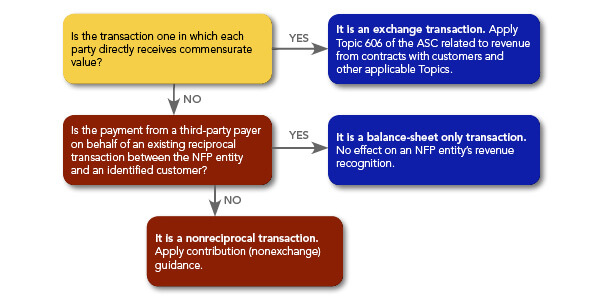

The proposed ASU would require a Not For Profit (NFP) entity to evaluate whether the resource provider is receiving direct commensurate value in return for the resources transferred (i.e. undertaking an exchange or reciprocal transaction). The proposed ASU notes the following:

- A resource provider (including a private foundation, a government agency, or other) is not synonymous with the general public. Indirect benefit received by the public as a result of the assets transferred is not equivalent to commensurate value received by the resource provider.

- Execution of a resource providers’ mission or the positive sentiment from acting as a donor would not constitute commensurate value received by a resource provider for purposes of determining whether a transfer of assets is a contribution or an exchange.

Consistent with current accounting principles generally accepted in the United States (GAAP), if the resource provider is not receiving direct value for the resources provided, the transaction will be considered a contribution (or nonreciprocal transaction), unless it can be shown that the resource provider is making the payment on behalf of an existing exchange transaction between the NFP entity and an identified customer.

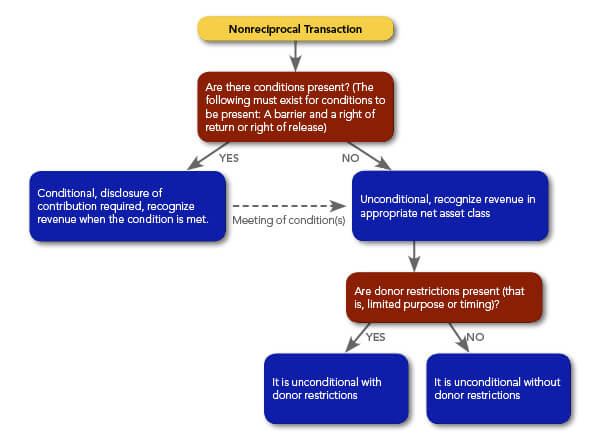

The ASU also provides guidance on whether a contribution is conditional or unconditional. This decision is based on whether a barrier that must be overcome and either a right of return of assets transferred or a right of release of a promisor’s obligation to transfer assets is determinable from the agreement (or another document referenced in the agreement). The presence of both a barrier and a right of return or a right of release indicates that a recipient NFP entity is not entitled to the transferred assets (or a future transfer of assets) until it has overcome the barriers in the agreement. Prior to overcoming those barriers, the contribution would be considered conditional.

After a contribution has been deemed unconditional, an entity would then consider whether the contribution is restricted on the basis of the current definition of the term donor-imposed restriction, which includes a consideration of how broad or narrow the purpose of the agreement is, and whether the resources are available for use only after a specified date.

The FASB believes that the proposed ASU could result in more grants and contracts being accounted for as contributions (often conditional contributions) than under current GAAP. For this reason, clarifying the guidance about whether a contribution is conditional or unconditional is important because such classification affects the timing of contribution revenue recognition. Recipients of conditional promises to give would be required to comply with current disclosure requirements in paragraph 958-310-50-4 of the ASC. Contributions are only recognized within the financial statements once they are considered unconditional.

For more information, please contact your Dean Dorton advisor or Simon Keemer at skeemer@deandorton.com.